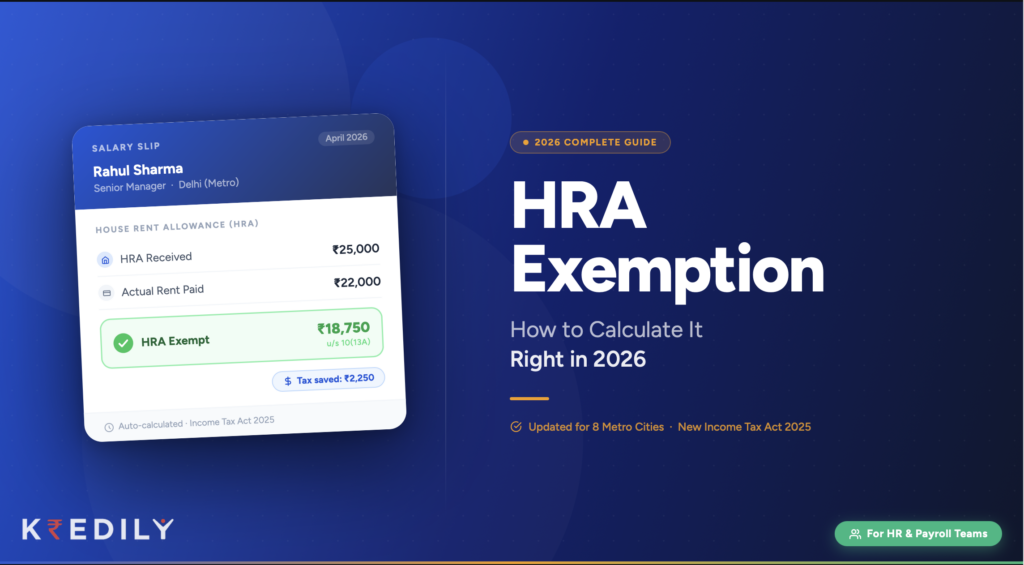

HRA Exemption: Formula, Calculation, Metro City Rules, and Everything HR Teams Need to Know

If you are a salaried employee, House Rent Allowance is very likely one of the largest components in your salary slip. And if your company has structured your CTC thoughtfully, HRA can also be one of the biggest legal tax savers available to you.

Yet many employees either claim it incorrectly or leave money on the table entirely. Many HR teams, especially those managing payroll manually, apply the wrong formula or overlook documentation requirements. The result is either excess TDS deduction or compliance risk at the time of assessment.

This guide covers everything you need to know about the HRA exemption. What it is, how it is calculated, which cities qualify for higher limits, what documents HR teams need to collect, and how salaried employees in the new tax regime should think about it.

Whether you are an employee trying to understand your tax benefit or an HR professional managing Form 12BB declarations, this article walks you through every detail.

What is HRA Exemption?

House Rent Allowance, commonly known as HRA, is a component that most employers include in employee salary structures. It is designed to compensate employees for the cost of renting accommodation near their workplace.

The tax benefit linked to HRA is called the HRA exemption. Under Section 10(13A) of the Income Tax Act, the portion of HRA that qualifies as exempt is not counted as taxable income. This means it directly reduces the amount on which you pay income tax.

To be clear about the terminology: HRA exemption is not a deduction. It is an exemption, which means the qualifying amount is excluded from gross taxable salary before any deductions are applied.

Three conditions must be true for you to claim HRA exemption:

First, you must be a salaried employee. Self-employed individuals cannot claim HRA exemption under Section 10(13A). They have a separate provision under Section 80GG.

Second, HRA must be a part of your salary structure. If your employer does not include HRA as a component in your CTC, you cannot claim this exemption.

Third, you must actually be paying rent for accommodation that you do not own. If you live in your own house, you are not eligible for HRA exemption even if HRA appears on your salary slip.

Quick Answer: HRA exemption allows salaried employees to exclude a portion of their House Rent Allowance from taxable income, provided they pay rent for accommodation they do not own. The exempt amount is the lowest of three calculated values.

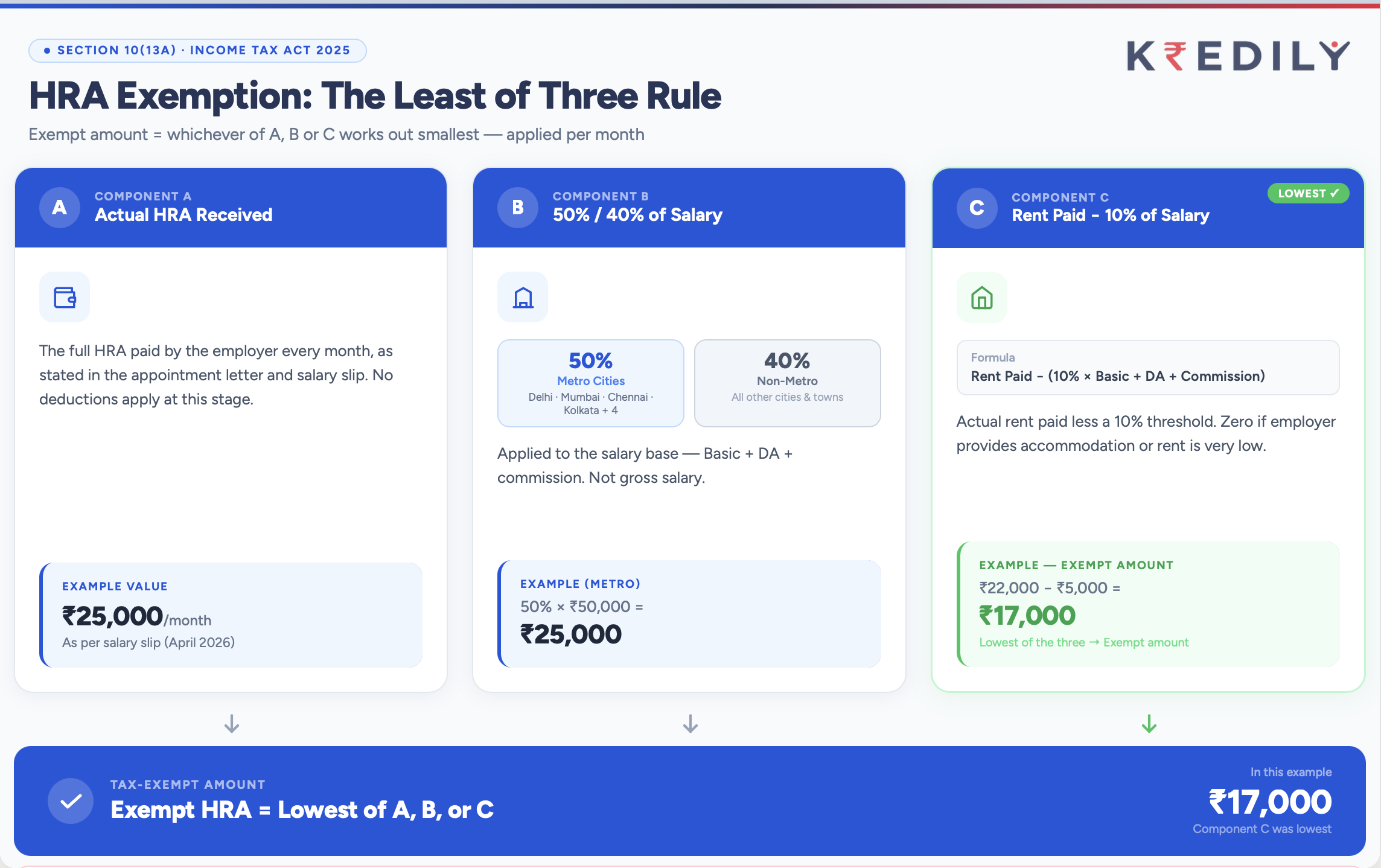

The HRA Exemption Formula (Step-by-Step Calculation)

The HRA exemption amount is always the lowest of the following three values. You calculate all three and take the minimum.

Value 1: Actual HRA received from your employer. This is the HRA amount your employer pays you, as shown on your salary slip.

Value 2: 50% of basic salary (for metro cities) or 40% of basic salary (for non-metro cities). Basic salary here includes dearness allowance if it forms part of your salary for retirement benefit calculations.

Value 3: Actual rent paid minus 10% of basic salary. This is the rent you actually pay each month multiplied by 12 (for the full year), minus 10% of your annual basic salary.

Formula written out:

HRA Exemption = Minimum of:

(a) Actual HRA received

(b) 50% of Basic Salary [metro] OR 40% of Basic Salary [non-metro]

(c) Actual Rent Paid minus 10% of Basic Salary

The logic behind this formula is straightforward. The government limits the benefit to genuine rent expenditure rather than the full HRA amount. Value (c) allows only the portion of rent that exceeds 10% of your salary to be considered. Meanwhile, value (b) limits the exemption based on whether you live in a metro or non-metro city. Finally, value (a) prevents the exemption from exceeding the HRA amount you actually received from your employer.

What Counts as Basic Salary in the HRA Formula?

Basic salary for the HRA formula includes your base pay plus any dearness allowance that forms part of pay for provident fund or retirement benefit purposes. It does not include HRA itself, special allowances, bonuses, or other variable components.

If your salary slip shows Basic: Rs. 40,000 and DA: Rs. 5,000 (forming part of retirement pay), your basic for HRA purposes is Rs. 45,000 per month or Rs. 5,40,000 annually.

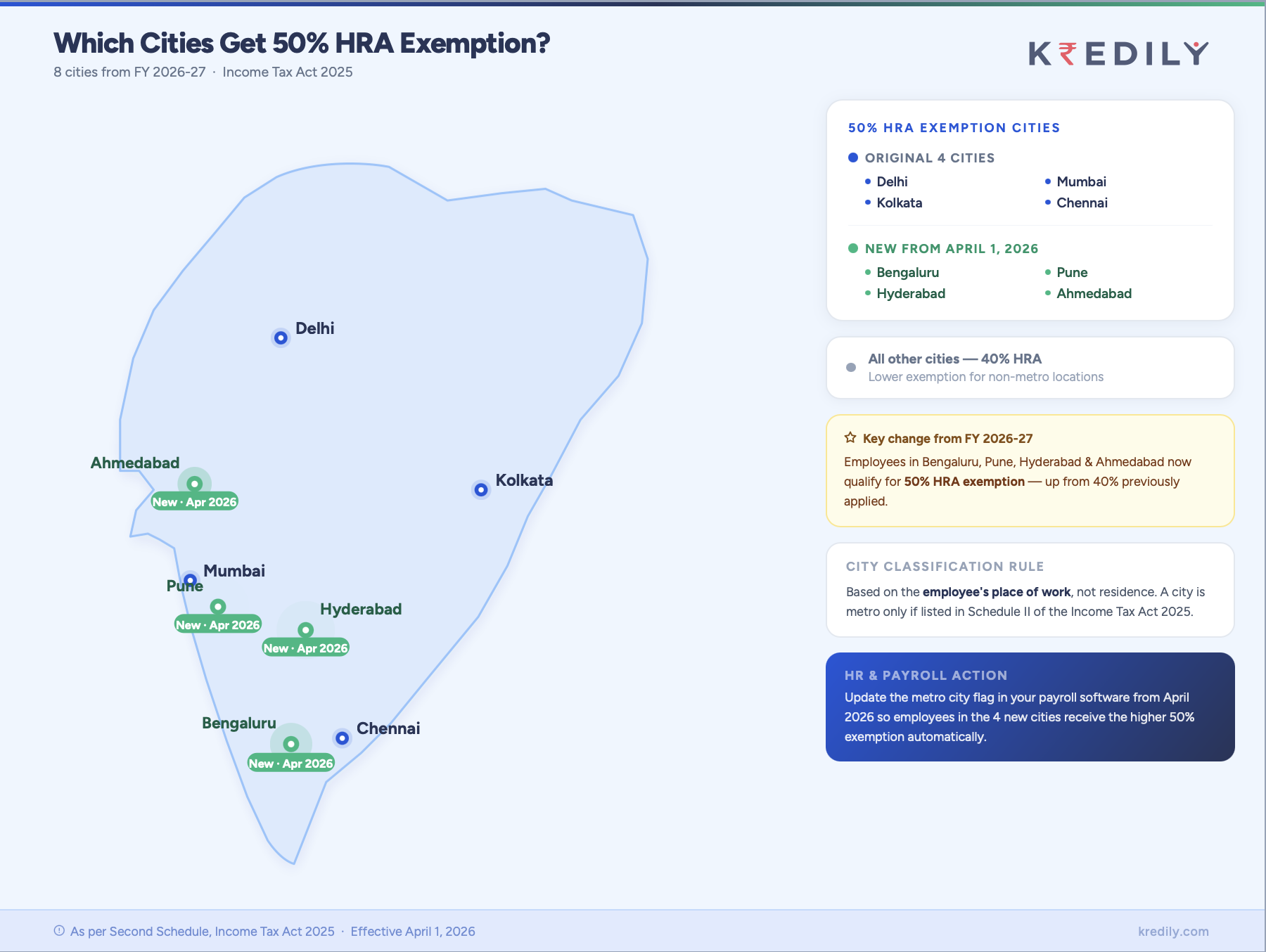

Metro vs Non-Metro: Which Cities Qualify for 50% HRA?

This is one of the most common sources of confusion among employees and HR teams.

| City | Metro Status | HRA Limit (% of Basic) |

|---|---|---|

| Delhi | Metro | 50% |

| Mumbai | Metro | 50% |

| Kolkata | Metro | 50% |

| Chennai | Metro | 50% |

| Bengaluru | Non-Metro | 40% |

| Hyderabad | Non-Metro | 40% |

| Pune | Non-Metro | 40% |

| Ahmedabad | Non-Metro | 40% |

| All other cities | Non-Metro | 40% |

Many employees working in Bengaluru or Hyderabad assume these are metro cities for tax purposes because of their size and cost of living. They are not. The classification is based on the original Income Tax Act provisions and has not been updated to reflect modern city growth.

The city classification is based on where you actually live and pay rent, not where your office is located. If you work in Gurgaon but rent accommodation there, Gurgaon falls under Delhi NCR and is treated as metro for HRA purposes. Always check the specific guidance for your city if you are in a satellite or border area.

HRA Exemption Calculation: Two Worked Examples

Let us walk through two practical examples so the formula becomes completely clear.

Example 1: Employee in Delhi (Metro City)

Ramesh works in Delhi. His salary details are:

| Component | Monthly | Annual |

|---|---|---|

| Basic Salary | Rs. 40,000 | Rs. 4,80,000 |

| HRA Received | Rs. 20,000 | Rs. 2,40,000 |

| Rent Paid | Rs. 18,000 | Rs. 2,16,000 |

Step 1: Value (a) — Actual HRA received Rs. 2,40,000

Step 2: Value (b) — 50% of Basic (metro) 50% of Rs. 4,80,000 = Rs. 2,40,000

Step 3: Value (c) — Rent paid minus 10% of Basic Rs. 2,16,000 minus 10% of Rs. 4,80,000 = Rs. 2,16,000 minus Rs. 48,000 = Rs. 1,68,000

HRA Exemption = Minimum of Rs. 2,40,000, Rs. 2,40,000, Rs. 1,68,000 = Rs. 1,68,000

Ramesh can claim Rs. 1,68,000 as exempt from income tax. The remaining HRA of Rs. 72,000 (Rs. 2,40,000 minus Rs. 1,68,000) will be added to his taxable salary.

Example 2: Employee in Bengaluru (Non-Metro City)

Priya works in Bengaluru. Her salary details are:

| Component | Monthly | Annual |

|---|---|---|

| Basic Salary | Rs. 50,000 | Rs. 6,00,000 |

| HRA Received | Rs. 22,000 | Rs. 2,64,000 |

| Rent Paid | Rs. 25,000 | Rs. 3,00,000 |

Step 1: Value (a) — Actual HRA received Rs. 2,64,000

Step 2: Value (b) — 40% of Basic (non-metro) 40% of Rs. 6,00,000 = Rs. 2,40,000

Step 3: Value (c) — Rent paid minus 10% of Basic Rs. 3,00,000 minus 10% of Rs. 6,00,000 = Rs. 3,00,000 minus Rs. 60,000 = Rs. 2,40,000

HRA Exemption = Minimum of Rs. 2,64,000, Rs. 2,40,000 = Rs. 2,40,000

Priya can claim Rs. 2,40,000 as exempt. Even though she pays more rent than her HRA, the non-metro cap limits her benefit to 40% of basic.

Notice something important here: Priya pays Rs. 3,00,000 in rent annually but can only claim Rs. 2,64,000 in HRA. Her claim is further capped at Rs. 2,40,000 by the city classification. This illustrates why the metro vs non-metro distinction matters significantly.

Who Is Eligible for HRA Exemption?

Not every employee can claim this benefit. Here is a clear checklist.

Who Can Claim HRA Exemption?

You can claim HRA exemption when all of the following conditions are met:

- You work as a salaried employee and HRA is included in your salary.

- You pay rent for a house that you do not own.

- The rented house is your primary residence.

- You have chosen the old tax regime for the financial year.

When HRA Exemption Does Not Apply

HRA exemption cannot be claimed in these situations:

- You live in a house that you own.

- HRA is part of your salary, but you do not pay any rent.

- You are self-employed. In this case, you may be eligible to claim a deduction under Section 80GG instead.

- You have opted for the new tax regime, where HRA exemption is not available.

An Important Exception Many People Miss

Paying rent to a parent or another close family member does not automatically make you ineligible for the HRA exemption. The rental arrangement must be genuine, supported by proper documentation, and the recipient should report the rental income on their income tax return. This is a valid and widely accepted practice when an employee lives in a property owned by a parent or another family member.

HRA Exemption Under Old vs New Tax Regime

This is a critical point that many employees miss when choosing their tax regime at the beginning of the financial year.

HRA exemption is available only under the old tax regime. If you opt for the new tax regime, which was made the default for most taxpayers, you cannot claim the HRA exemption at all.

Under the new regime, tax slabs are lower, and most exemptions and deductions are removed. This is a tradeoff: you pay tax on a higher gross income but at lower rates.

| Feature | Old Tax Regime | New Tax Regime |

|---|---|---|

| HRA Exemption | Available | Not available |

| Standard Deduction | Rs. 50,000 | Rs. 75,000 (from FY 2024-25) |

| Section 80C | Available | Not available |

| Home Loan Interest (Sec 24) | Available | Not available |

| Professional Tax | Deductible | Not deductible |

For employees paying significant rent in high-cost cities, the old regime often works out better because the HRA exemption alone can reduce taxable income by Rs. 2 to 3 lakh or more annually.

The best approach is to calculate your tax liability under both regimes at the start of the financial year and choose accordingly. Your HR or payroll team should help you with this comparison using your actual numbers. You can also use Kredily’s payroll system to run a side-by-side comparison automatically.

Documents HR Teams Must Collect for HRA Compliance

If you manage payroll for a company, HRA compliance involves collecting proper documentation from employees at the start of the year and verifying it before adjusting TDS calculations.

Form 12BB is the primary document. Every employee claiming HRA exemption must submit a duly filled Form 12BB to their employer before the beginning of the financial year or before their first salary is processed.

Rent receipts are mandatory when the annual rent exceeds Rs. 1 lakh. If an employee pays more than Rs. 1,00,000 in rent per year (roughly Rs. 8,333 per month), the employer must collect rent receipts and also obtain the landlord’s PAN. Without the landlord’s PAN, the employer cannot allow the exemption for amounts above Rs. 1 lakh annually.

Rent agreement as supporting evidence. While not always mandatory, a signed rent agreement strengthens the claim and protects both the employee and the employer in case of scrutiny.

Documents HR should collect and retain:

| Document | When Required |

|---|---|

| Form 12BB (signed) | Always |

| Rent receipts (monthly) | Always |

| Landlord PAN card copy | Rent over Rs. 1 lakh/year |

| Rent agreement | Recommended for all |

| Self-declaration if the landlord is a family member | When paying rent to a parent or a relative |

A critical HR responsibility: If the employee’s situation changes mid-year (they move cities, rent changes, or they buy a house), Form 12BB must be revised. The employer must adjust TDS accordingly for the remaining months of the year.

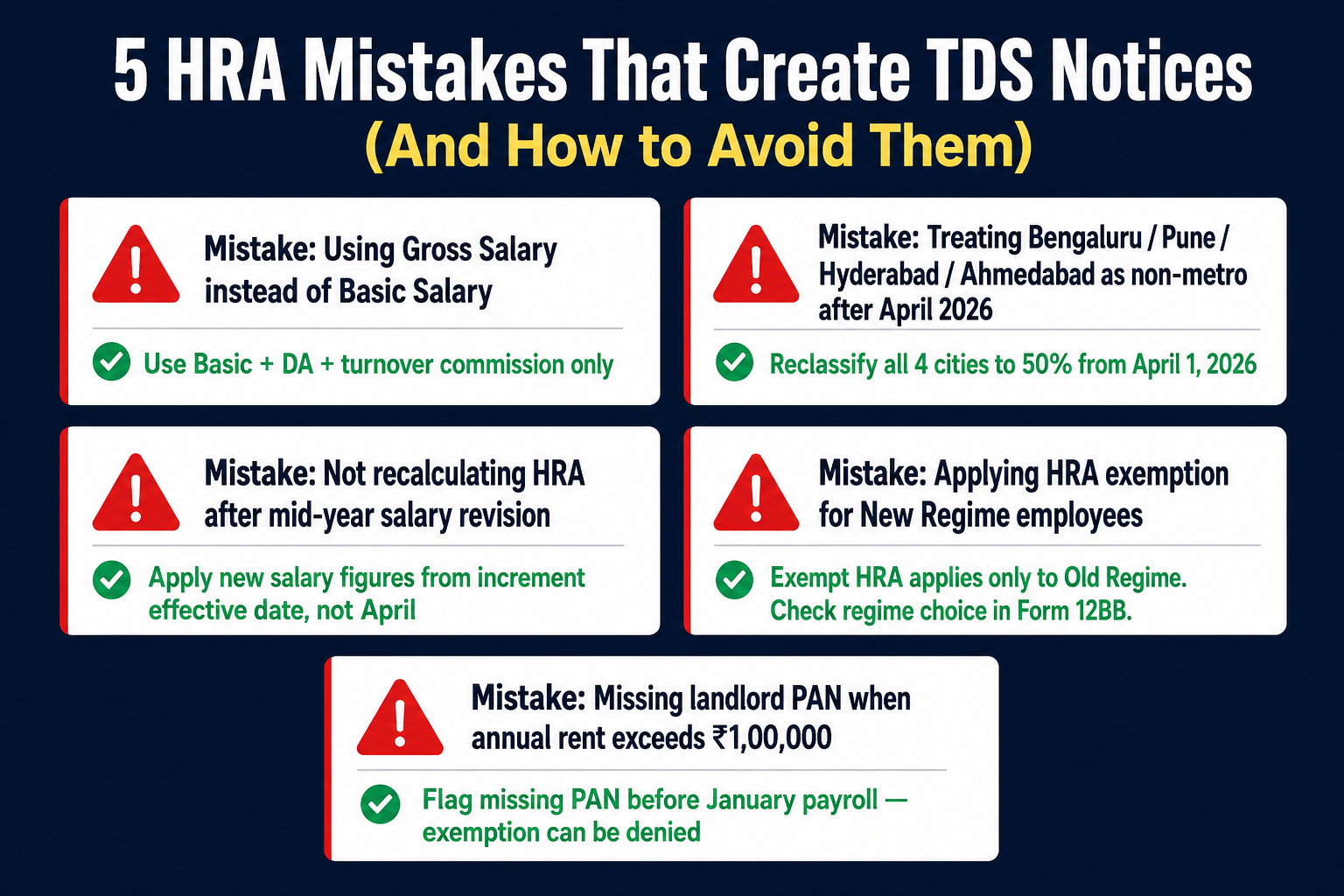

Common HRA Mistakes HR Teams and Employees Make

These are the most common HRA-related errors we see across payroll audits.

Mistake 1: Applying the Metro Cap to Non-Metro Employees

HR teams sometimes apply 50% of basic salary for employees working in Bengaluru, Hyderabad, or Pune, incorrectly treating them as metro cities. The correct limit is 40%. This creates an inflated exemption and excess TDS shortfall at year-end.

Mistake 2: Not Collecting the Landlord PAN for High Rents

When an employee pays rent above Rs. 8,333 per month, HR must collect the landlord’s PAN. If this is missed, the employer faces compliance risk and the employee may not get the benefit they expected.

Mistake 3: Allowing HRA for Employees on the New Tax Regime

Some payroll systems or HR teams inadvertently apply the HRA exemption for employees who have opted for the new tax regime. This is not permissible. Any employee on the new regime must be taxed on their full HRA as part of their gross salary.

>

Mistake 4: Not Updating Form 12BB When Rent Changes

Employees who shift accommodation or change their rent amount mid-year must submit a revised Form 12BB. HR teams that rely on the initial submission without updates create mismatches that surface at the year-end tax reconciliation.

Mistake 5: Accepting Incomplete Rent Receipts

Rent receipts must include the landlord’s name, address, signature, amount, date, and a revenue stamp for amounts above Rs. 5,000 per receipt. Receipts that are missing any of these details may not hold up during assessment.

HRA When You Pay Rent to a Parent or Family Member

This is a legitimate tax planning option, but it comes with specific conditions that must be followed carefully.

You can pay rent to a parent or a family member and claim the HRA exemption on it. The arrangement must be genuine. The parent must own the property. The rent must be transferred by bank transfer or cheque, not cash, to create a paper trail.

The parent must declare the rent received as income under the head “Income from House Property” in their own income tax return. They can claim a standard deduction of 30% on that income, which reduces their tax liability.

For example, if Ananya pays her mother Rs. 15,000 per month in rent for staying in her mother’s house, Ananya can claim HRA exemption on that amount. Her mother must show Rs. 1,80,000 as rental income in her return and can deduct Rs. 54,000 (30%) as standard deduction, leaving a taxable amount of Rs. 1,26,000.

If the parent has little or no other income, this arrangement can result in significant net tax savings for the family as a whole.

However, you cannot pay rent to a spouse and claim an HRA exemption. The Income Tax Department does not allow HRA claims where rent is paid to a husband or wife.

How Payroll Software Handles HRA Exemption

For HR and payroll professionals, manually calculating HRA exemption for every employee every month is error-prone and time-consuming. Modern payroll platforms automate this entirely.

When an employee submits their Form 12BB declaration with rent amount and city, a payroll system like Kredily automatically:

Applies the correct metro or non-metro percentage based on the city entered. Runs the three-value minimum comparison each month. Adjusts TDS deduction to reflect the exempt portion. Flags any missing PAN information for rent above the threshold. Generates a reconciliation report at year-end.

This removes the risk of manual calculation errors and ensures every employee gets their correct HRA benefit without the HR team having to verify each calculation individually.

For companies with employees spread across multiple cities, this automation matters even more because the metro and non-metro rules need to be applied differently for different employees simultaneously.

Kredily’s payroll module handles multi-city salary structures and HRA declarations out of the box.

HRA and Home Loan Interest: Can You Claim Both?

A common question from employees who have taken a home loan is whether they can claim both HRA exemption and home loan interest deduction simultaneously.

The answer is yes, under specific conditions.

If you have taken a home loan on a property that you do not currently live in (for example, you bought a flat in another city but continue to rent accommodation near your current workplace), you can claim:

HRA exemption for the rent you pay at your current location. Home loan interest deduction under Section 24(b) for the EMI interest on your property.

Both claims are valid because they relate to different properties and different purposes. You are renting where you work and owning where you have invested.

However, if you own a property in the same city where you work and pay rent on a different property in the same city, the Income Tax Department may question your HRA claim during assessment. You would need a strong justification for why you are renting rather than living in your owned property.

For employees in the old tax regime who have both a home loan and HRA, their salary package can offer substantial combined deductions.

Frequently Asked Questions About HRA Exemption

What is the maximum HRA exemption I can claim?

There is no fixed maximum cap in rupees. The exemption is limited by whichever of the three formula values is the lowest. In practice, for metro city employees, the cap tends to be 50% of basic salary. For non-metro employees, it is 40% of basic salary, assuming that figure is lower than the actual rent paid minus 10% of basic.

Can I claim HRA exemption if I do not have rent receipts?

Officially, rent receipts are required documentation for claiming HRA from your employer. For amounts below Rs. 1 lakh annually, some flexibility exists, but it is always safer to maintain proper receipts. Without receipts, your employer is not obligated to allow the exemption, and the Income Tax Department may disallow it during scrutiny.

Is the HRA exemption available to government employees?

Yes. Government employees are eligible for HRA exemption on the same terms as private sector employees, provided they pay rent and their salary structure includes HRA.

What if I pay rent, but my employer does not give me HRA?

If your salary structure does not include HRA but you pay rent, you can claim a deduction under Section 80GG. The deduction limit is the lowest of: Rs. 5,000 per month, 25% of total income, or actual rent paid minus 10% of total income. You cannot claim 80GG if you receive HRA from your employer.

Does HRA exemption apply to PG accommodation or hostel fees?

Yes, rent paid for paying guest accommodation qualifies for HRA exemption, provided it is a genuine tenancy arrangement and you have receipts. Hostel fees paid to a licensed residential hostel may also qualify, though this depends on the nature of the arrangement and documentation.

Can I claim HRA if I work from home and my home is rented?

Yes. Even if you work from home, if you are a salaried employee paying rent for the accommodation, HRA exemption applies. The work-from-home arrangement does not affect eligibility.

What happens to HRA under the new tax regime?

Under the new tax regime, HRA exemption is not available. The full HRA you receive is treated as taxable income. The trade-off is that the new regime offers lower tax slab rates. Employees must decide at the start of the financial year which regime suits them better based on their overall tax situation.

Can my employer reject my HRA claim even if I submit all documents?

Your employer can reject or reduce the claim if the submitted documents are incomplete or appear incorrect. For example, if rent receipts are missing signatures, lack a revenue stamp, or the landlord PAN is absent for high-value rent, the employer may not process the exemption. Always submit complete documentation.

Is HRA exemption calculated monthly or annually?

Technically the benefit is computed annually, but payroll systems apply it monthly for TDS purposes. Your employer estimates your total HRA exemption for the year and divides the tax savings across each salary payment. A final reconciliation happens in February or March to ensure accuracy before Form 16 is issued.

What is the difference between HRA exemption and an HRA deduction?

HRA exemption under Section 10(13A) directly reduces your gross taxable salary before deductions are applied. A deduction, like those under Chapter VIA (such as 80C, 80D), reduces taxable income after the gross figure is determined. HRA exemption is structurally more beneficial because it reduces the base on which all subsequent calculations are made.

Manage HRA Compliance Automatically with Kredily

Manual HRA calculations create risk. Whether it is applying the wrong metro rate, missing a landlord PAN, or failing to update TDS when an employee moves cities, small errors compound quickly across a team of 50, 100, or 500 employees.

Kredily’s payroll platform handles the full HRA workflow automatically. Employees declare their rent details once. The system calculates exemptions, adjusts TDS, flags missing documents, and reconciles at year-end.

Start a free trial and see how Kredily simplifies HRA and payroll compliance for your team.

Wrapping Up

HRA exemption is one of the most straightforward tax benefits available to salaried employees, but only when it is calculated correctly and backed by proper documentation. The formula involves three simple comparisons and the lower of the three becomes the exempt amount.

The city classification also plays an important role. Employees living in metro cities can claim HRA based on 50% of their basic salary, whereas those in non-metro cities are limited to 40%. However, anyone who chooses the new tax regime cannot claim HRA exemption at all. Therefore, HR teams must collect Form 12BB, rent receipts, and landlord PAN details before processing monthly payroll to ensure accurate tax calculations and maintain compliance.

Getting HRA right protects employees from excess TDS deduction and protects employers from compliance gaps. A good payroll system makes all of this automatic.