When Rohan joined a Bengaluru-based startup as their first HR hire, one of his earliest payroll runs had a problem. He had correctly computed basic pay, HRA, and PF. He had missed professional tax entirely. Nobody had told him it varied by state. Nobody had told him his company needed a separate registration certificate for it. The first employee complaint arrived within three days of salary credit.

Professional tax is one of those compliance requirements that looks simple on paper but creates real problems when ignored. It is state-controlled, which means the slab rates, deadlines, and registration requirements differ from Maharashtra to Karnataka to Tamil Nadu. An HR team managing payroll across multiple offices has to get each state right, separately.

This guide covers every active state’s professional tax slab for 2026-27, how to calculate it correctly, employer registration requirements, deposit deadlines, and the most common mistakes HR teams make, so you can avoid all of them.

What Is Professional Tax in India?

Professional tax is a direct tax levied by state governments on individuals who earn a salary or practise a profession, trade, or employment within that state. It is one of the few taxes in India that falls entirely within state jurisdiction.

Despite the word “professional” in its name, this tax applies to all salaried employees, not only those in white-collar roles. A factory worker in West Bengal and a software engineer in Karnataka both pay it, though the slabs and rates differ significantly.

The Constitutional Basis of Professional Tax

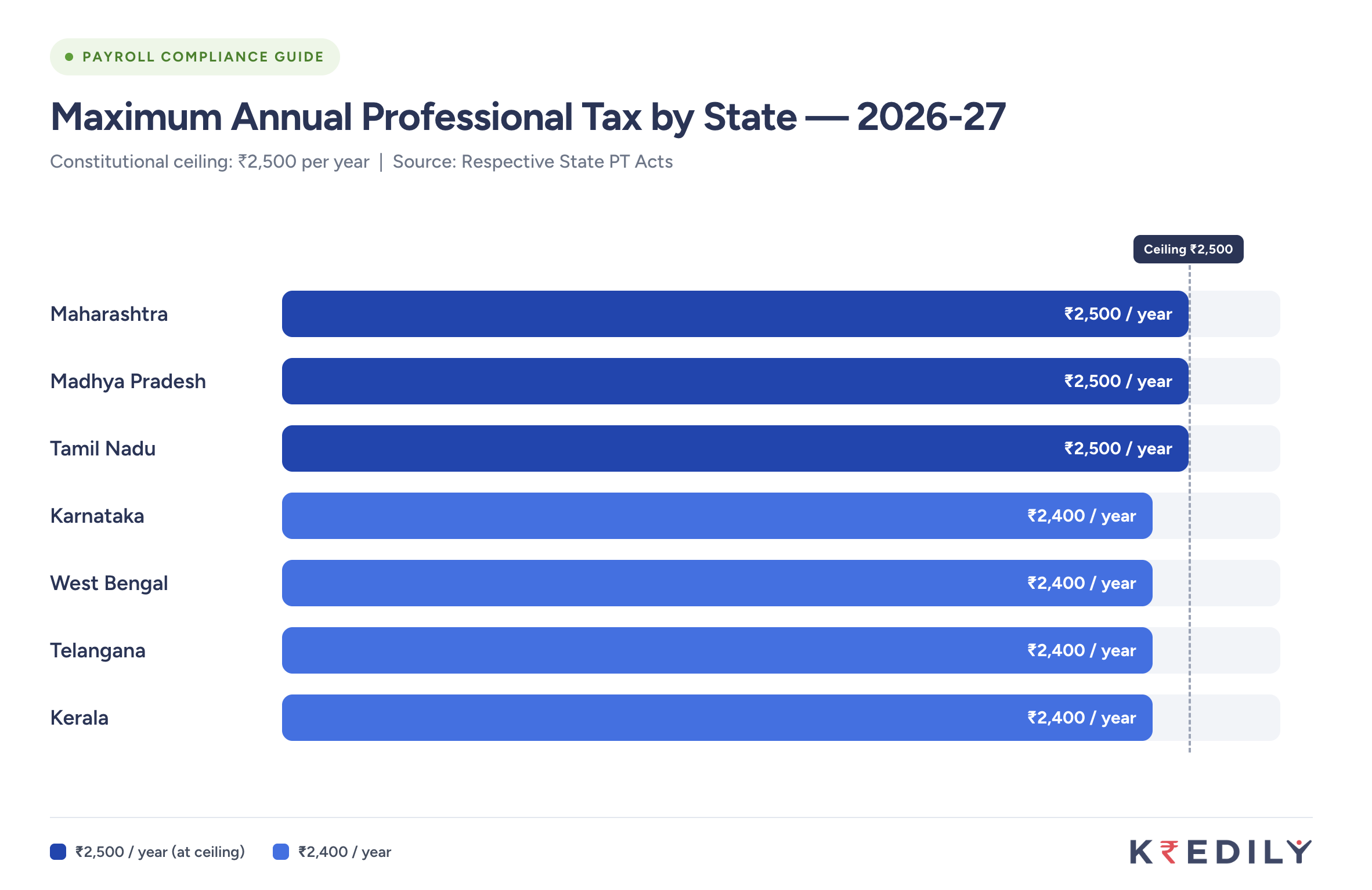

Article 246 of the Indian Constitution, read with Schedule VII, gives state legislatures the authority to levy taxes on professions, trades, callings, and employment. Article 276 sets the ceiling: no state can levy professional tax exceeding Rs. 2,500 per year on any individual.

This ceiling of Rs. 2,500 per year has remained unchanged since 1988, though several states operate well below it. The constitutional cap means professional tax will never grow beyond a nominal deduction, regardless of how high an employee’s salary goes.

Who Pays Professional Tax?

Professional tax applies to three categories of people:

Salaried employees in states that levy PT: The employer deducts it from the monthly salary and deposits it with the state government on the employee’s behalf.

Self-employed individuals and freelancers: Professionals such as doctors, lawyers, chartered accountants, architects, and consultants who practise within a PT-levying state must register independently and pay directly.

Business owners and directors: In some states, the company itself pays a nominal professional tax on behalf of its directors or partners.

Which States Levy Professional Tax in 2026?

Not all Indian states levy professional tax. Below is the current status for every state and union territory.

| State / UT | PT Applicable | Maximum Annual PT |

|---|---|---|

| Maharashtra | Yes | Rs. 2,500 |

| Karnataka | Yes | Rs. 2,400 |

| West Bengal | Yes | Rs. 2,400 |

| Andhra Pradesh | Yes | Rs. 2,400 |

| Telangana | Yes | Rs. 2,400 |

| Tamil Nadu | Yes | Rs. 1,200 (half-yearly) |

| Kerala | Yes | Rs. 2,400 (half-yearly) |

| Gujarat | Yes | Rs. 2,400 |

| Madhya Pradesh | Yes | Rs. 2,500 |

| Odisha | Yes | Rs. 2,400 |

| Assam | Yes | Rs. 2,040 |

| Meghalaya | Yes | Rs. 2,500 |

| Tripura | Yes | Rs. 1,500 |

| Jharkhand | Yes | Rs. 2,500 |

| Bihar | Yes | Rs. 2,500 |

| Sikkim | Yes | Nominal rates |

| Goa | Yes | Nominal rates |

| Puducherry | Yes | Nominal rates |

| Delhi | No | Not applicable |

| Haryana | No | Not applicable |

| Rajasthan | No | Not applicable |

| Uttar Pradesh | No | Not applicable |

| Punjab | No | Not applicable |

| Himachal Pradesh | No | Not applicable |

| Uttarakhand | No | Not applicable |

| Chandigarh (UT) | No | Not applicable |

If your business is registered in a non-PT state, employees working from that state are not liable for professional tax — even if the parent company is headquartered in Maharashtra or Karnataka.

Professional Tax Slab Rates State-Wise 2026-27

Maharashtra Professional Tax Slab 2026-27

Maharashtra uses the monthly salary as the basis for professional tax calculation. Note the unusual February rule: employees earning above Rs. 10,000 are charged Rs. 300 in February and Rs. 200 in all other months, which brings the annual total to Rs. 2,500.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 7,500 | Nil |

| Rs. 7,501 to Rs. 10,000 | Rs. 175 |

| Above Rs. 10,000 | Rs. 200 (Rs. 300 in February) |

Annual maximum: Rs. 2,500

Karnataka Professional Tax Slab 2026-27

Karnataka’s slabs are tiered and cover a broad salary range. Employees earning below Rs. 25,000 per month pay PT at lower rates.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 25,000 | Nil |

| Rs. 25,001 to Rs. 41,666 | Rs. 150 |

| Rs. 41,667 to Rs. 83,333 | Rs. 200 |

| Above Rs. 83,333 | Rs. 200 |

Annual maximum: Rs. 2,400

Note: Karnataka revised its slabs in 2023, increasing the nil threshold significantly. Many HR systems still carry the old Rs. 15,000 nil threshold. Verify your payroll software reflects the updated slabs.

West Bengal Professional Tax Slab 2026-27

West Bengal calculates professional tax on monthly salary and follows a tiered structure.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 10,000 | Nil |

| Rs. 10,001 to Rs. 15,000 | Rs. 110 |

| Rs. 15,001 to Rs. 25,000 | Rs. 130 |

| Rs. 25,001 to Rs. 40,000 | Rs. 150 |

| Above Rs. 40,000 | Rs. 200 |

Annual maximum: Rs. 2,400

Andhra Pradesh Professional Tax Slab 2026-27

Andhra Pradesh bases professional tax on monthly salary with the following slabs.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 15,000 | Nil |

| Rs. 15,001 to Rs. 20,000 | Rs. 150 |

| Above Rs. 20,000 | Rs. 200 |

Annual maximum: Rs. 2,400

Telangana Professional Tax Slab 2026-27

Telangana follows slabs very similar to Andhra Pradesh. The state separated from AP in 2014 and has maintained its own PT structure since then.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 15,000 | Nil |

| Rs. 15,001 to Rs. 20,000 | Rs. 150 |

| Above Rs. 20,000 | Rs. 200 |

Annual maximum: Rs. 2,400

Tamil Nadu Professional Tax Slab 2026-27

Tamil Nadu is a half-yearly state. PT is calculated and deposited every six months, not monthly. The slabs are based on half-yearly income.

| Half-Yearly Salary | PT Per Half Year |

|---|---|

| Up to Rs. 21,000 | Nil |

| Rs. 21,001 to Rs. 30,000 | Rs. 135 |

| Rs. 30,001 to Rs. 45,000 | Rs. 315 |

| Rs. 45,001 to Rs. 60,000 | Rs. 690 |

| Rs. 60,001 to Rs. 75,000 | Rs. 1,025 |

| Above Rs. 75,000 | Rs. 1,250 |

Annual maximum: Rs. 2,500 (Rs. 1,250 × 2 halves)

Employers deposit in September and March each year. Missing either deadline attracts interest and penalties.

Kerala Professional Tax Slab 2026-27

Kerala is also a half-yearly state. PT is deposited in June and December.

| Half-Yearly Salary | PT Per Half Year |

|---|---|

| Up to Rs. 11,999 | Nil |

| Rs. 12,000 to Rs. 17,999 | Rs. 120 |

| Rs. 18,000 to Rs. 29,999 | Rs. 180 |

| Rs. 30,000 to Rs. 44,999 | Rs. 360 |

| Rs. 45,000 to Rs. 59,999 | Rs. 600 |

| Rs. 60,000 to Rs. 74,999 | Rs. 900 |

| Rs. 75,000 to Rs. 99,999 | Rs. 1,200 |

| Rs. 1,00,000 and above | Rs. 1,200 |

Annual maximum: Rs. 2,400

Gujarat Professional Tax Slab 2026-27

Gujarat levies professional tax based on monthly salary.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 5,999 | Nil |

| Rs. 6,000 to Rs. 8,999 | Rs. 80 |

| Rs. 9,000 to Rs. 11,999 | Rs. 150 |

| Rs. 12,000 and above | Rs. 200 |

Annual maximum: Rs. 2,400

Madhya Pradesh Professional Tax Slab 2026-27

Madhya Pradesh calculates professional tax on the monthly salary. It is another half-yearly deposit state, with filings due in June and December.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 18,750 | Nil |

| Rs. 18,751 to Rs. 25,000 | Rs. 125 |

| Rs. 25,001 to Rs. 33,333 | Rs. 167 |

| Above Rs. 33,333 | Rs. 208 |

Annual maximum: Rs. 2,500

Odisha Professional Tax Slab 2026-27

Odisha levies professional tax monthly on gross salary.

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 13,304 | Nil |

| Rs. 13,305 to Rs. 25,000 | Rs. 125 |

| Rs. 25,001 to Rs. 41,666 | Rs. 167 |

| Above Rs. 41,666 | Rs. 208 |

Annual maximum: Rs. 2,500

Assam Professional Tax Slab 2026-27

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 10,000 | Nil |

| Rs. 10,001 to Rs. 14,999 | Rs. 150 |

| Rs. 15,000 to Rs. 24,999 | Rs. 170 |

| Above Rs. 25,000 | Rs. 170 |

Annual maximum: Rs. 2,040

Meghalaya Professional Tax Slab 2026-27

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 4,999 | Nil |

| Rs. 5,000 to Rs. 7,999 | Rs. 35 |

| Rs. 8,000 to Rs. 11,999 | Rs. 75 |

| Rs. 12,000 to Rs. 17,999 | Rs. 125 |

| Rs. 18,000 to Rs. 29,999 | Rs. 175 |

| Above Rs. 30,000 | Rs. 208 |

Annual maximum: Rs. 2,500

Tripura Professional Tax Slab 2026-27

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 7,500 | Nil |

| Rs. 7,501 to Rs. 15,000 | Rs. 56 |

| Rs. 15,001 to Rs. 25,000 | Rs. 112 |

| Above Rs. 25,000 | Rs. 125 |

Annual maximum: Rs. 1,500

Jharkhand Professional Tax Slab 2026-27

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 25,000 | Nil |

| Rs. 25,001 to Rs. 41,667 | Rs. 100 |

| Above Rs. 41,667 | Rs. 208 |

Annual maximum: Rs. 2,500

Bihar Professional Tax Slab 2026-27

| Monthly Gross Salary | PT Per Month |

|---|---|

| Up to Rs. 25,000 | Nil |

| Rs. 25,001 to Rs. 41,666 | Rs. 83 |

| Above Rs. 41,666 | Rs. 208 |

Annual maximum: Rs. 2,500

States Where Professional Tax Does Not Apply

If your employees work from any of these locations, you do not deduct professional tax from their salary: Delhi, Uttar Pradesh, Haryana, Rajasthan, Punjab, Himachal Pradesh, Uttarakhand, Arunachal Pradesh, Manipur, Mizoram, Nagaland, Jammu and Kashmir, Ladakh, Dadra and Nagar Haveli, Daman and Diu, Lakshadweep, and Andaman and Nicobar Islands.

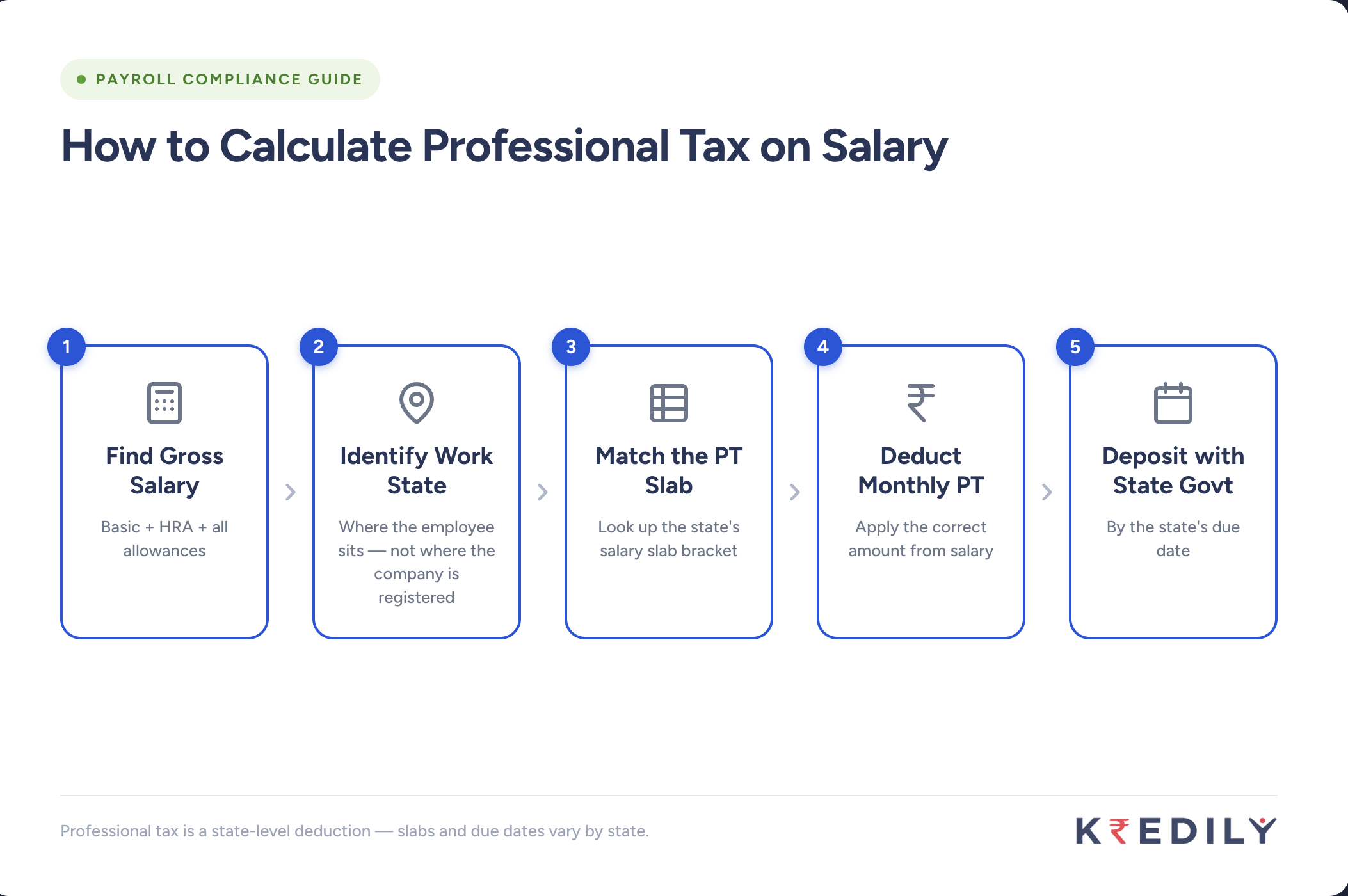

How Professional Tax Is Calculated on Salary

Professional tax is always calculated on gross salary, which includes basic pay, HRA, special allowance, and other allowances, before any deductions such as PF or income tax.

Step-by-Step Calculation

- Determine the gross monthly salary of the employee.

- Identify the state where the employee is physically working (not where the company is registered).

- Find the appropriate slab from that state’s PT schedule.

- Deduct the corresponding PT amount from the employee’s monthly salary.

- Deposit the collected amount with the state government by the due date.

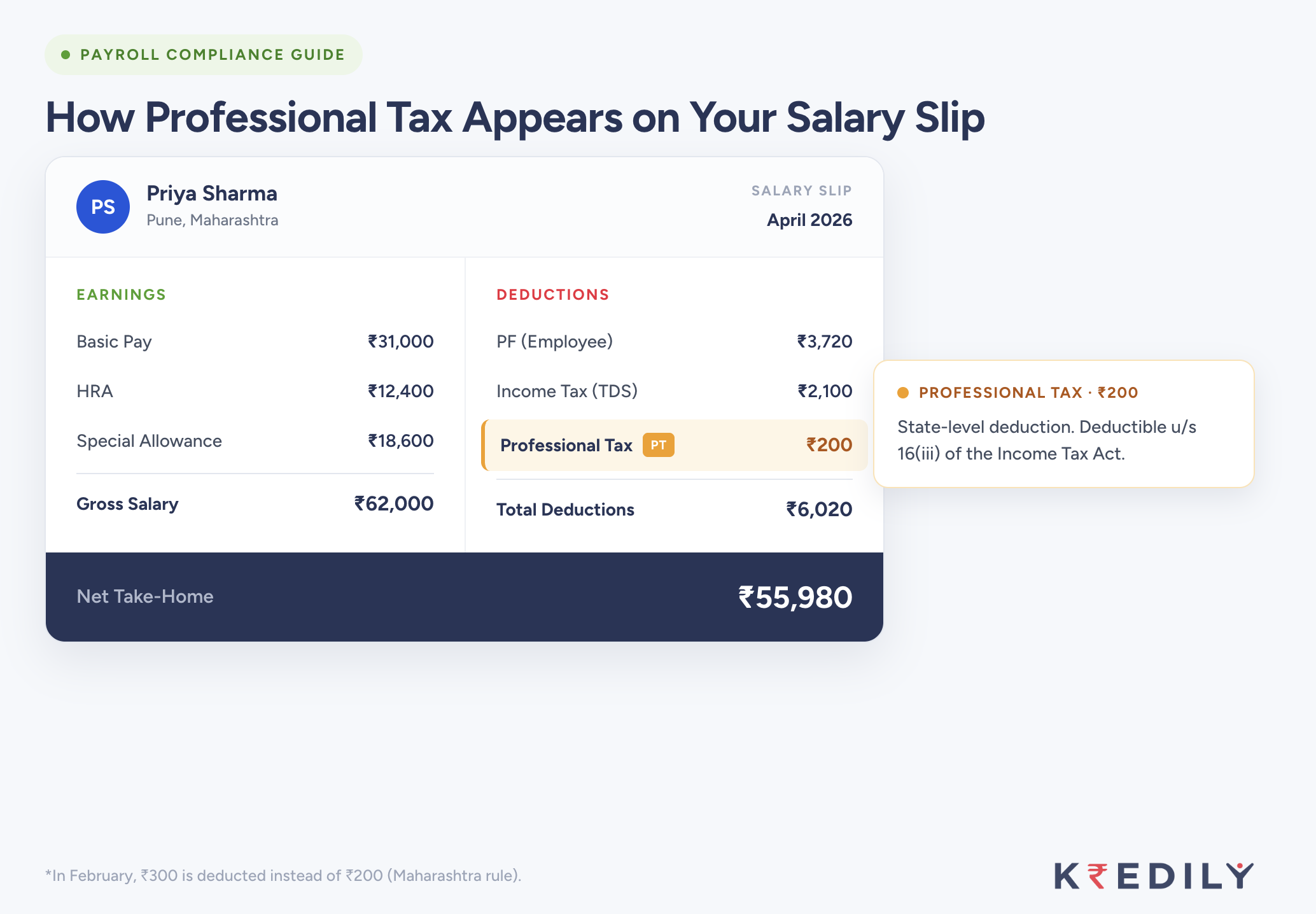

Worked Example: Employee in Pune (Maharashtra)

Priya works in Pune. Her gross monthly salary is Rs. 62,000.

In Maharashtra, any employee earning above Rs. 10,000 per month pays Rs. 200 per month, and Rs. 300 in February.

So Priya’s professional tax is: Rs. 200 per month from April to January = Rs. 2,000, Rs. 300 in February = Rs. 300, Rs. 200 in March = Rs. 200. Annual PT = Rs. 2,500

Her salary slip shows a deduction of Rs. 200 under “Professional Tax” for all months except February, which shows Rs. 300. The total annual deduction stays capped at Rs. 2,500.

Worked Example: Employee in Bengaluru (Karnataka)

Arjun works in Bengaluru. His gross monthly salary is Rs. 38,000.

Karnataka’s revised slab shows that employees earning up to Rs. 25,000 pay nil. Since Arjun earns Rs. 38,000, which falls in the Rs. 25,001 to Rs. 41,666 bracket, his monthly PT is Rs. 150.

Annual PT = Rs. 150 × 12 = Rs. 1,800

How Professional Tax Appears on the Salary Slip

On a standard salary slip, professional tax appears as a deduction, usually labelled “Professional Tax” or “PT” or “Prof. Tax.” It sits alongside other statutory deductions such as PF and income tax. The net take-home salary is calculated after subtracting all three.

Employees sometimes ask HR why this deduction exists when they already pay income tax. The answer is that professional tax is separate from income tax. One is central; the other is state-level. The good news is that the full amount of professional tax paid in a year is deductible under Section 16(iii) of the Income Tax Act, which reduces taxable income modestly.

Professional Tax for Mid-Month Joiners and Exit Month

This is one of the most commonly mishandled areas in payroll.

When an employee joins mid-month, say on the 18th, their gross salary for that month is proportional. If a Maharashtra employee earns Rs. 62,000 per month and joins on the 18th, their first-month salary is roughly Rs. 28,000. Since this figure still exceeds Rs. 10,000, Maharashtra PT applies at Rs. 200.

However, some states apply PT based on the prorated salary, which can push the employee into a lower slab or even the nil bracket for that month. The safest approach is to check whether the state calculates PT on the actual monthly salary drawn or on the fixed monthly CTC.

For exit months, if an employee is serving notice and receives a partial month’s salary, the same logic applies. Most payroll software handles this automatically. If you are processing manually, compare the actual amount paid in that month against the slab thresholds.

Professional Tax for Self-Employed and Freelancers

If you are a freelancer, consultant, doctor, lawyer, or chartered accountant practising in a PT-levying state, you are responsible for your own professional tax registration and payment.

The process typically involves:

- Visit the state’s commercial tax or professional tax department website.

- Register as a self-employed professional under the state’s PT Act.

- Obtain a PT enrollment certificate (EC).

- File returns and pay PT annually or as specified by the state.

Self-employed individuals in states like Maharashtra, Karnataka, and West Bengal must proactively enroll. There is no employer to deduct and deposit on their behalf. Penalties for non-registration accumulate over time and can be substantial.

Who Is Exempt from Professional Tax?

Several categories of individuals are fully or partially exempt from professional tax across most states.

Parents or guardians of a child with a permanent disability are exempt in most states. The exemption typically applies to one parent.

Individuals above 65 years of age are exempt in many states, including Maharashtra and Karnataka.

Members of the armed forces — including the army, navy, and air force serving in the state — are exempt from PT in most states.

Women earning below a specified threshold are exempt in some states. Maharashtra, for example, exempts all women employees with a monthly salary up to Rs. 10,000.

Individuals suffering from a permanent physical disability, including blindness, are exempt in most PT-levying states.

Badli workers in textile industries and certain daily wage workers may also qualify for exemption, depending on the state.

Always verify exemption eligibility with the specific state’s PT rules, because the categories and income thresholds differ.

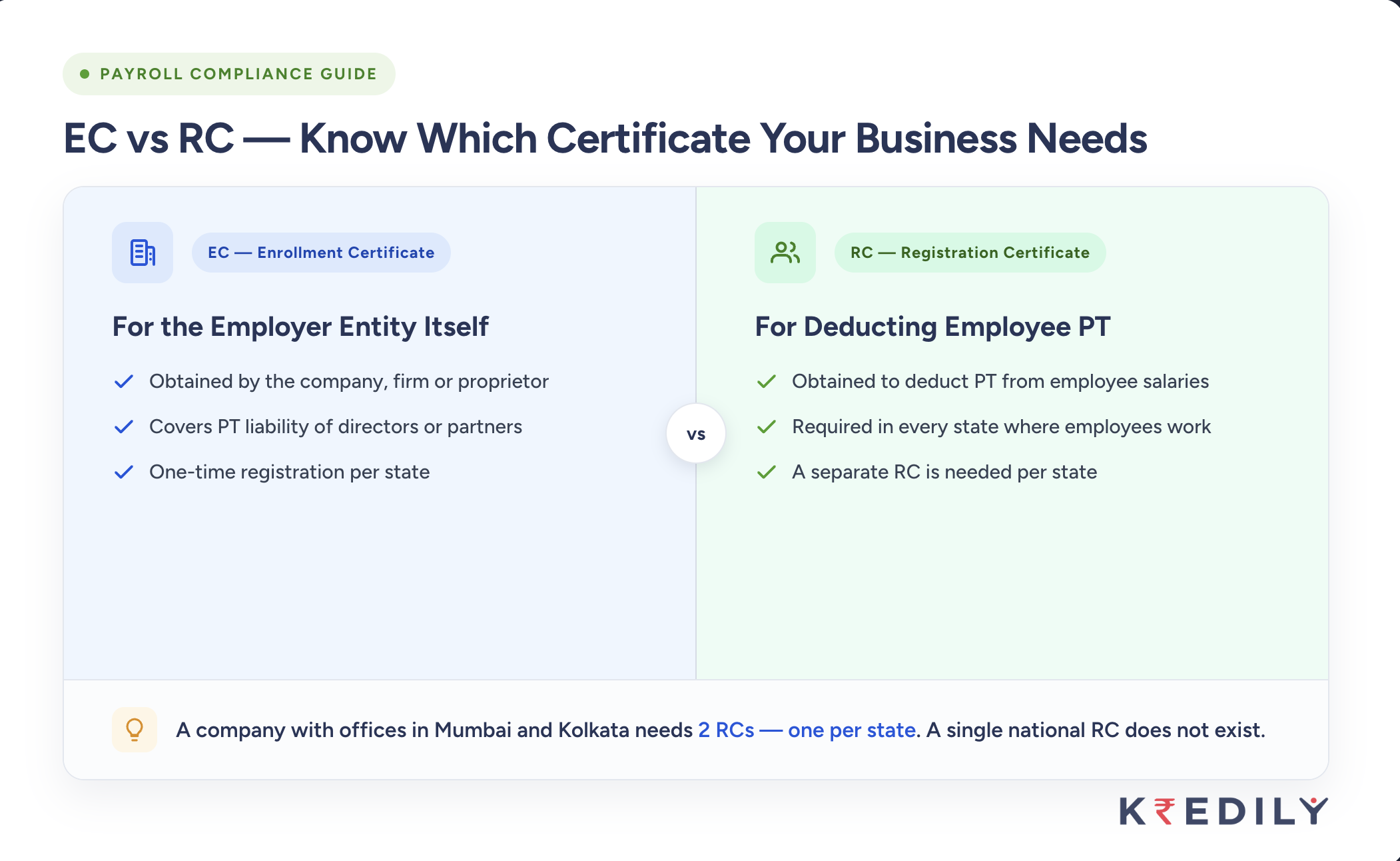

Employer Registration: EC vs RC — Know the Difference

This distinction trips up many HR professionals, especially those managing PT compliance for the first time.

There are two types of certificates under professional tax law:

Enrollment Certificate (EC): An EC is obtained by the employer for itself. If the company is registered in a PT-levying state, it must get an EC and pay professional tax on behalf of each of its directors, partners, or proprietors. This is the company’s own PT liability.

Registration Certificate (RC): An RC is what the employer obtains in order to deduct and deposit professional tax on behalf of its employees. Every company that employs salaried staff in a PT-levying state must hold an RC for that state.

So a company with 50 employees in Maharashtra needs: One EC for the company itself (or its directors). One RC to deduct and deposit PT on behalf of those 50 employees.

If your company has offices in both Karnataka and West Bengal, you need separate RC registrations in each state. A single national registration does not exist because professional tax is a state-level levy.

For detailed guidance on compliance registration processes, see our post on how HR software helps leaders navigate compliance challenges.

Employer Obligations and Deposit Deadlines by State

An employer’s professional tax obligations do not end at deduction. Registration, monthly or half-yearly deposit, and annual return filing are all required.

The core responsibilities are:

First, register under the applicable state PT Act and obtain an RC before running the first payroll in that state.

Second, deduct the correct PT amount from each employee’s salary every month based on that employee’s gross salary and the applicable state slab.

Third, deposit the collected PT with the state government by the due date specific to that state.

Fourth, file periodic returns as required by the state. Most states require an annual return. Some require monthly or quarterly statements.

State-Wise PT Deposit Deadlines

| State | Frequency | Due Date |

|---|---|---|

| Maharashtra | Monthly | Last day of the month |

| Karnataka | Monthly | 20th of the following month |

| West Bengal | Monthly | Last day of the month |

| Andhra Pradesh | Monthly | 10th of the following month |

| Telangana | Monthly | 10th of the following month |

| Tamil Nadu | Half-yearly | September 30 and March 31 |

| Kerala | Half-yearly | June 30 and December 31 |

| Gujarat | Monthly | Last day of the month |

| Madhya Pradesh | Half-yearly | June 30 and December 31 |

| Odisha | Monthly | Last day of the month |

| Assam | Monthly | Last day of the month |

Note: Deadlines shift when the last day falls on a public holiday. Always verify the current state gazette for the applicable year. Late deposits attract interest typically at 1 to 2 percent per month and a separate penalty.

Consequences of Non-Compliance

Failing to register for professional tax in a state where you have employees is not a minor oversight. The consequences are concrete.

Late payment interest: States typically charge 1 to 2 percent per month on the outstanding PT amount.

Penalty for non-registration: Most states impose a fixed penalty for failure to obtain an RC within the stipulated time, ranging from Rs. 1,000 to Rs. 5,000 per month of default.

Penalty for non-filing of returns: Annual return defaults attract additional penalties, sometimes proportional to the number of employees.

Legal action: Persistent defaults can lead to recovery proceedings under the applicable state PT Act, which may include attaching company bank accounts.

For a broader view of compliance requirements that your startup or SME should track, refer to our Annual Compliance Checklist for Startups and SMEs in India.

Professional Tax vs Income Tax: Key Differences

Employees and even some HR professionals occasionally confuse professional tax with income tax. They are separate levies with very different characteristics.

| Parameter | Professional Tax | Income Tax |

|---|---|---|

| Levied by | State government | Central government |

| Applicable to | Employees in PT states only | All taxpayers across India |

| Rate | Fixed slab-based; max Rs. 2,500 per year | Progressive slab based on total income |

| Who deducts | Employer (for salaried employees) | Employer via TDS |

| Filing responsibility | Employer files state PT returns | Individual files ITR |

| Tax benefit | Fully deductible under Section 16(iii) | N/A |

| Basis | Gross monthly salary | Annual taxable income |

| Uniformity | Varies by state | Uniform across India |

The most important point for employees to understand is the last row in the deduction column. The professional tax deducted from their salary reduces their taxable income under the Income Tax Act. If an employee paid Rs. 2,400 in professional tax during the year, their taxable income is reduced by exactly Rs. 2,400 when computing income tax liability.

To understand how all payroll deductions interact together, our post on payroll deductions for employers and employees in India covers this in detail.

What HR Managers Get Wrong About Professional Tax

After reviewing dozens of payroll audits and compliance checklists, these are the six most common professional tax mistakes HR teams make.

Mistake 1: Using the employee’s state of residence instead of the state of work. Professional tax applies based on where the employee physically works, not where they live. A remote employee working from their home in Pune pays Maharashtra PT, even if the company is headquartered in Bengaluru.

Mistake 2: Not updating Karnataka’s revised nil threshold. Karnataka raised its nil threshold to Rs. 25,000 per month in 2023. Many payroll systems still apply PT to employees earning between Rs. 15,000 and Rs. 25,000, resulting in incorrect deductions. Verify your payroll software’s Karnataka slab configuration.

Mistake 3: Missing the Maharashtra February rule. Maharashtra charges Rs. 300 in February instead of the usual Rs. 200 for employees above Rs. 10,000. Payroll software should handle this automatically, but manual payroll often misses it. The annual total should be Rs. 2,500, not Rs. 2,400.

Mistake 4: Applying PT to employees in non-PT states. If an employee works from Delhi or Haryana, there is no professional tax to deduct. Deducting PT from such employees is an incorrect payroll entry that requires reversal.

Mistake 5: Registering only in the company’s state and ignoring remote worker states. If your company is in Mumbai but three employees work from West Bengal, you need an RC in West Bengal too. Remote work has made multi-state PT compliance far more common.

Mistake 6: Treating PT as a one-time setup task. State governments occasionally revise slabs, thresholds, and deadlines. Karnataka’s 2023 revision is an example. HR teams need a process to monitor state-wise PT rule changes annually.

For a comprehensive look at HR compliance pitfalls, you may find our guide on avoiding common HR mistakes useful reading alongside this one.

How Kredily Handles Professional Tax Automatically

Managing professional tax across multiple states manually is genuinely difficult. The state-by-state slab differences, varying deposit deadlines, and the February Maharashtra quirk are all detail-level rules that create errors in manual payroll.

Kredily’s payroll engine applies the correct professional tax slab for each employee based on their work location state automatically. When you add an employee in Karnataka, Kredily applies Karnataka’s slab. When a Pune-based employee’s salary changes and crosses a Maharashtra threshold, the deduction updates in the next payroll run without any manual intervention. The February Rs. 300 rule for Maharashtra runs automatically.

For companies with employees across multiple states, Kredily manages separate RC compliance and generates state-wise PT reports for filing.

You can explore how Kredily handles professional tax and full payroll compliance for businesses like yours— no setup fee, free to get started.

Frequently Asked Questions on Professional Tax Slab

What is the maximum professional tax in India?

The constitutional ceiling under Article 276 is Rs. 2,500 per year. No state can levy more than this amount from any individual. Maharashtra is the only state that reaches exactly Rs. 2,500 annually. Most other states cap out between Rs. 1,200 and Rs. 2,400.

Is professional tax deductible from income tax?

Yes. The full amount of professional tax paid during the financial year is allowed as a deduction from gross salary under Section 16(iii) of the Income Tax Act. If you paid Rs. 2,400 in professional tax, your taxable income is reduced by Rs. 2,400 before applying income tax slabs.

Does professional tax apply to employees working from home?

Yes, but it depends on the state where the employee is physically located, not where the company is registered. A remote employee working from their home in Kolkata pays West Bengal professional tax, regardless of where the employer is based.

Is professional tax applicable in Delhi?

No. Delhi does not levy professional tax. Employees whose primary work location is Delhi do not have any professional tax deducted from their salary.

How is professional tax different from payroll tax?

Professional tax is a state-level deduction from an employee’s salary based on salary slabs. Payroll tax in the Indian context refers more broadly to employer-side contributions such as PF and ESI. Professional tax is deducted from the employee’s salary; the employer merely collects and deposits it. For a full breakdown of the different taxes involved in payroll, see our post on demystifying payroll tax.

What happens if an employer does not deduct professional tax?

The employer remains responsible for depositing the correct PT amount with the state government regardless of whether the deduction was made from the employee’s salary. Failure to deposit results in interest charges, penalties, and potential recovery action by the state authority.

Can professional tax slabs change every year?

Yes. State governments have the authority to revise professional tax slabs, thresholds, and rates, subject to the Rs. 2,500 annual ceiling. Karnataka’s 2023 revision of the nil threshold is a recent example. HR teams should verify slab rates at the start of each financial year.