What Is Form 24Q In TDS? Meaning, Purpose And Who Must File It

Form 24Q is a quarterly TDS return filed by employers to report tax deducted from employee salaries under Section 192 of the Income Tax Act, 1961. Employers submit this return to the Income Tax Department to declare salary payments, tax deductions, and challan details for the taxes deposited with the government. As a result, the tax deducted from employees is properly recorded and reflected in their tax records. Employers must file This form every quarter if they deduct TDS on salary payments.

TDS on salary is governed by Section 192 of the Income Tax Act, which requires employers to deduct tax before paying employee salaries. Therefore, once the tax is deducted, the employer must deposit it with the government and report the details through this In addition, this process helps maintain transparency in salary tax compliance and ensures that employee tax credits appear correctly in their Form 26AS.

Any employer responsible for deducting TDS on salaries must file Form 24Q. For example, this includes companies, LLPs, partnership firms, startups, proprietorship businesses, and government organizations that pay taxable salaries to employees. Therefore, filing this return becomes part of the employer’s tax compliance responsibility and helps the Income Tax Department track salary-based TDS deductions across organizations.

Form 24Q Due Dates And Quarterly Compliance Requirements

Employers who deduct TDS on employee salaries must file every quarter as part of their payroll tax compliance. The Income Tax Department requires organizations to report salary payments and tax deductions through this quarterly TDS return. Therefore, employers must ensure that they submit the return within the prescribed deadlines to avoid penalties or compliance issues.

Under Rule 31A of the Income Tax Rules, employers must file Form 24Q four times during a financial year. Each return reports the salary TDS deducted for a specific quarter and confirms that the employer has deposited the tax with the government. In addition, the final quarter return includes detailed salary computation information that supports the generation of Form 16 for employees.

The standard Form 24Q due dates for each financial quarter are listed below:

| Quarter | Period | Due Date |

|---|---|---|

| Q1 | April – June | 31 July |

| Q2 | July – September | 31 October |

| Q3 | October – December | 31 January |

| Q4 | January – March | 31 May |

Employers must follow these deadlines carefully because the Income Tax Department monitors quarterly TDS return filings for compliance. As a result, timely submission of Form helps organizations maintain accurate salary tax records and avoid late filing fees under the Income Tax Act.

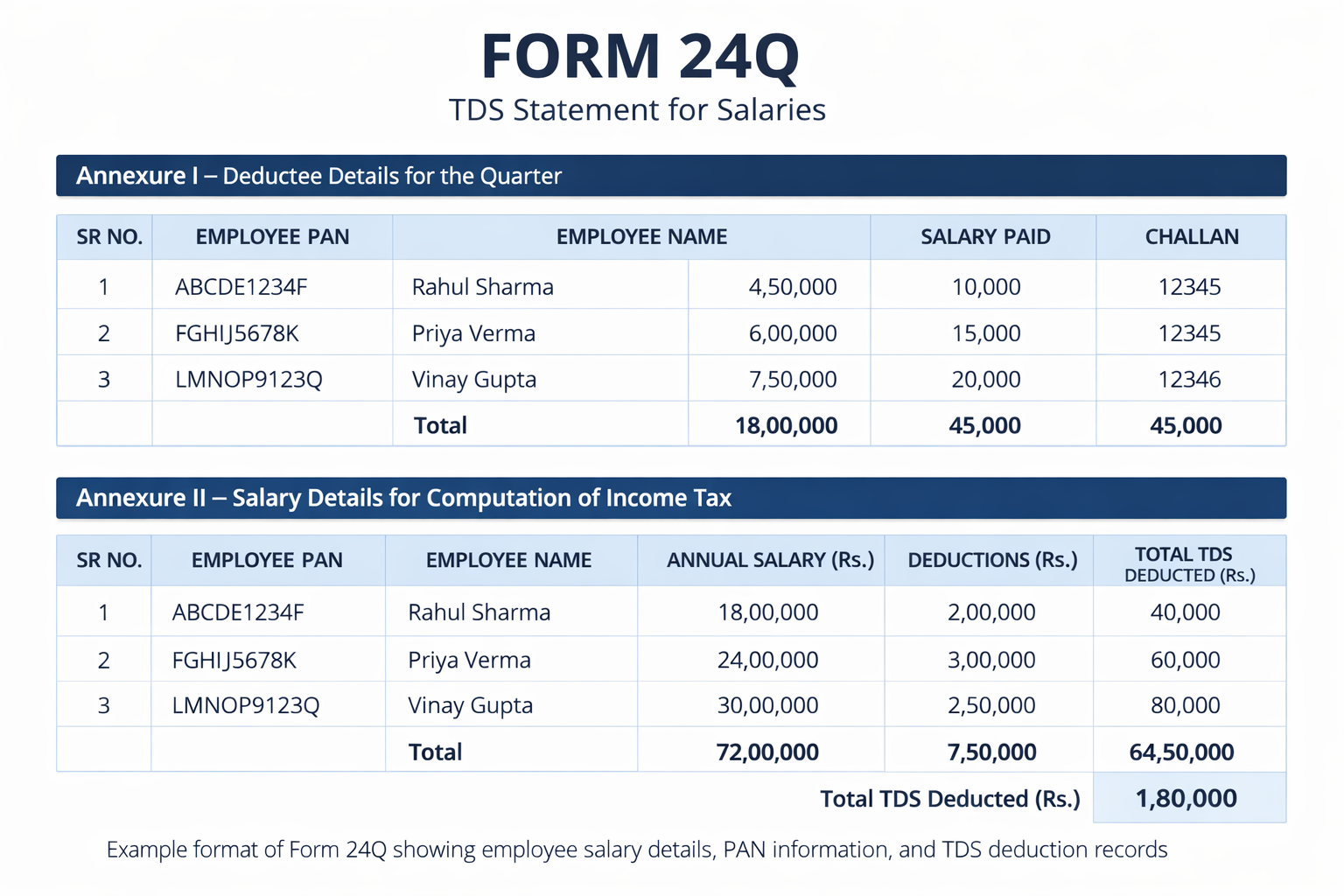

Structure of Form 24Q: Annexure I and Annexure II Explained

Form 24Q follows a structured format used by the Income Tax Department to report tax deducted at source (TDS) on employee salaries. Employers must include complete details of salary payments, employee PAN information, and the TDS deposited with the government. Therefore, understanding the structure of this could helps employers file accurate quarterly TDS returns and maintain payroll tax compliance.

The return mainly contains two important sections: Annexure I and Annexure II. Each annexure records different salary and tax information required under the Income Tax Act.

Annexure I – Quarterly TDS Details

Annexure I contains the details of TDS deducted during a specific quarter. Employers submit this annexure every quarter when filing Form 24Q.

It generally includes:

-

Employer details and TAN

-

Employee PAN

-

Salary paid during the quarter

-

TDS deduction details

-

Challan details of tax deposited with the government

As a result, Annexure I allows the Income Tax Department to track quarterly salary payments and verify that the employer has deposited the correct tax amount.

Annexure II – Annual Salary Computation

Annexure II contains the complete salary computation of employees for the financial year. Employers submit this annexure only in the fourth quarter return (January–March).

It usually includes:

-

Annual salary breakup

-

Exemptions and deductions

-

Taxable income calculation

-

Final TDS computation under Section 192

Therefore, Annexure II ensures that the total tax deducted from employees during the year matches the final salary computation.

Together, Annexure I and Annexure II provide a complete record of employee salary details, PAN information, TDS deductions, and challan deposits. This structured format helps employers maintain payroll tax compliance and ensures that employee tax credits appear correctly in Form 26AS.

Form 24Q Filing Process: Step-by-Step Guide for Employers

Employers who deduct tax from employee salaries must file Form 24Q every quarter to report TDS under Section 192 of the Income Tax Act. The filing process involves preparing the return, validating the data, and submitting it through the government portal. Therefore, employers must follow the correct steps to ensure accurate reporting and avoid compliance issues.

Below is the standard Form 24Q filing process followed by most organizations.

Step 1: Prepare the return using Return Preparation Utility (RPU)

Employers first prepare the TDS return using the Return Preparation Utility (RPU) provided by the TIN-NSDL portal. This utility allows employers to enter details such as employer information, employee PAN, salary payments, and TDS deduction details for the relevant quarter.

Step 2: Validate the file using File Validation Utility (FVU)

After preparing the return, the file must be validated using the File Validation Utility (FVU). This tool checks the data for formatting errors, missing details, or inconsistencies. As a result, validation ensures that the return meets the technical requirements set by the Income Tax Department.

Step 3: Upload the return through the TRACES / TIN-NSDL portal

Once the file is validated, employers can upload the Form 24Q return through the TRACES portal or the TIN-NSDL TDS return filing system. The uploaded file contains all salary TDS details for the relevant quarter.

Step 4: Submit the return using a Digital Signature Certificate (DSC)

Employers must authenticate the uploaded return using a Digital Signature Certificate (DSC). This step confirms the authenticity of the filing and ensures secure submission to the Income Tax Department.

Step 5: Generate the acknowledgment receipt

After successful submission, the system generates an acknowledgment receipt. Employers should save this receipt as proof of filing the quarterly TDS return.

Form 24Q Penalties, Errors and Correction Return Process

Employers who deduct tax at source from employee salaries must file Form 24Q every quarter to report the tax deducted under Section 192 of the Income Tax Act. The return helps the Income Tax Department track salary payments and ensure that the correct tax has been deposited with the government. Therefore, employers must submit accurate information and file the return within the prescribed due dates. Failure to do so may result in penalties and compliance notices.

Penalties for Late Filing or Incorrect Returns

If an employer fails to file Form on time or submits incorrect information, penalties may apply under the Income Tax Act. The most common penalties are related to late filing fees and incorrect TDS return reporting.

The penalties applicable to Form 24Q are summarized below:

| Situation | Applicable Section | Penalty Details |

|---|---|---|

| Late filing of Form 24Q | Section 234E | A late filing fee of ₹200 per day applies from the due date until the return is filed. However, the total fee cannot exceed the amount of TDS reported in the return. |

| Incorrect or delayed TDS return | Section 271H | The Income Tax Department may impose a penalty ranging from ₹10,000 to ₹1,00,000 if the return is filed late or contains incorrect information. |

However, the penalty under Section 271H may not apply if the employer files the return within one year of the due date, deposits the correct TDS amount, and pays the late filing fee under Section 234E.

Common Errors While Filing Form 24Q

Employers often face issues while filing TDS returns due to incorrect or incomplete information. These mistakes may lead to return rejection or compliance notices from the Income Tax Department.

Some common errors include:

-

PAN mismatch between employee records and tax database

-

Challan mismatch in the TDS payment details

-

Short deduction of TDS on employee salaries

-

Incorrect salary details or tax computation errors

-

Missing or incorrect employee information

Therefore, employers should carefully verify all payroll and tax details before submitting the return.

Correction Return or Revised Form 24Q

If errors are identified after filing the return, employers can submit a TDS correction return to revise the original Form 24Q. This process allows organizations to correct details such as employee PAN information, challan data, salary records, or TDS deduction amounts.

The revised return can be filed through the TRACES portal, which allows employers to update incorrect information in previously submitted returns. As a result, filing a correction return helps maintain accurate TDS records and prevents future compliance issues.

How Form 24Q Works in Payroll: Salary TDS, Challan Payment and Form 16 Generation

Payroll tax compliance involves several steps, including salary calculation, tax deduction, government payment, and reporting through TDS returns. Employers must follow this structured process to ensure that employee taxes are deducted correctly and reported to the Income Tax Department. Understanding how this workflow operates helps organizations maintain accurate payroll compliance and avoid reporting errors.

The process usually begins with employee salary calculation during monthly payroll processing. At this stage, employers determine the taxable income of each employee after considering salary components, exemptions, and declared deductions. Based on this calculation, the employer deducts Tax Deducted at Source (TDS) from the employee’s salary under Section 192 of the Income Tax Act.

Once the tax amount is deducted, the employer must deposit the collected TDS with the government. This payment is made through Challan ITNS 281, which is the official challan used for depositing TDS with the Income Tax Department. In most cases, organizations deposit this amount on a monthly basis as part of their payroll tax obligations.

Generate Form 24Q

↓

TDS deduction from salary under Section 192

↓

Monthly TDS payment to the government using Challan ITNS 281

↓

Employee tax deduction and challan details recorded in the payroll system

↓

Quarter-wise tracking of employee TDS and challan mapping

↓

Preparation of quarterly Form 24Q return data

↓

Generation of Form 16 for employees

↓

TDS details reflected in employee Form 26AS

After the employer deposits the tax and submits the quarterly Form 24Q return, the Income Tax Department updates the employee’s tax records. As a result, the deducted tax becomes visible in the employee’s Form 26AS, which acts as a consolidated statement of taxes paid.

In addition, the information reported in the quarterly return helps employers generate Form 16, the official certificate of TDS deducted from salary. Organizations provide this document to employees at the end of the financial year so they can accurately file their income tax returns.

Therefore, this workflow connects salary processing, TDS deduction, challan payments, government reporting, and employee tax documentation. Following this structured process helps employers maintain payroll compliance while ensuring that employees receive the correct tax credits in their records.

Automating Form 24Q with Payroll or HRMS Software

Managing salary tax compliance manually can be complex, especially for organizations with multiple employees and frequent payroll updates. Employers must calculate salary, deduct the correct tax, deposit the TDS with the government, and file quarterly returns such as Form 24Q. Therefore, relying only on spreadsheets or manual processes may increase the risk of calculation errors, missed deadlines, or incorrect reporting.

Modern payroll software and HRMS platforms help organizations simplify these compliance tasks by automating the payroll and tax reporting workflow. These systems integrate employee salary data, tax deductions, and government filing requirements into a single platform. As a result, employers can manage payroll compliance more efficiently while reducing manual work.

One of the key benefits of payroll software is automatic TDS calculation. The system calculates tax deductions based on employee salary details, exemptions, and investment declarations. In addition, employees can submit their investment declarations and tax-saving details through the HRMS platform. This information helps employers calculate the correct tax liability under Section 192 of the Income Tax Act.

Automation also helps generate accurate Form 24Q reports required for quarterly TDS return filing. Payroll systems organize employee salary data, PAN details, and tax deduction records in a structured format that supports easy preparation of TDS returns. Consequently, employers can generate the required reports without manually compiling payroll data.

Another important advantage is the availability of compliance reminders and alerts. Payroll systems notify employers about upcoming TDS payment deadlines, quarterly filing dates, and required documentation. As a result, organizations can avoid late filing penalties and maintain consistent payroll compliance.

By integrating TDS automation, payroll processing, and compliance tracking, HRMS platforms help employers manage salary tax reporting more accurately. This approach reduces administrative effort while ensuring that payroll data, tax deductions, and TDS returns remain consistent throughout the financial year.

FAQ (Frequently asked Questions)

Who needs to file Form 24Q?

Any employer who deducts TDS on employee salaries under Section 192 of the Income Tax Act must file Form 24Q. This applies to companies, LLPs, partnerships, proprietors, and government organizations.

How many times is Form 24Q filed in a year?

Form 24Q is filed four times a year, once for each financial quarter: April–June, July–September, October–December, and January–March.

What details are included in Form 24Q?

Form 24Q includes employer details, employee PAN, salary payments, TDS deducted, and challan details of the tax deposited with the government.

Can Form 24Q be revised after submission?

Yes, employers can file a correction return to fix errors such as incorrect PAN, challan mismatches, or wrong salary details.

What is the penalty for late filing of Form 24Q?

A late fee of ₹200 per day applies under Section 234E until the return is filed. Additional penalties may apply under Section 271H for incorrect or delayed filing.