What Is ESI Calculation And How Does It Work?

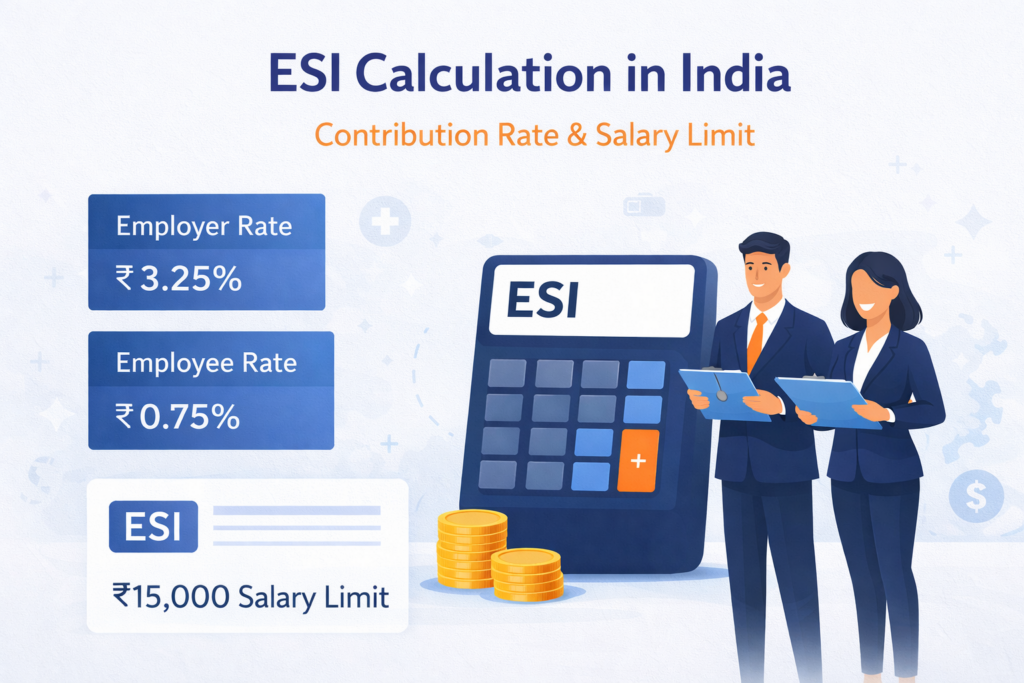

ESI calculation refers to the method used to determine the monthly contribution paid toward the Employee State Insurance scheme based on an employee’s gross wages. Under current ESIC rules, employees earning ₹21,000 or less per month are eligible for Its coverage. From this wage amount, the employee contributes 0.75% of gross salary, while the employer contributes 3.25%. Together, these contributions make up the total ESI contribution of 4% of the employee’s gross wages, which is deposited monthly with the Employees’ State Insurance Corporation (ESIC).

The calculation is applied to wages that fall within the eligibility limit and is typically processed during payroll. Employers deduct the employee’s share from the salary and add their own contribution before submitting the total amount to ESIC. This process ensures employees receive access to benefits such as medical care, sickness benefits, and insurance coverage under the scheme.

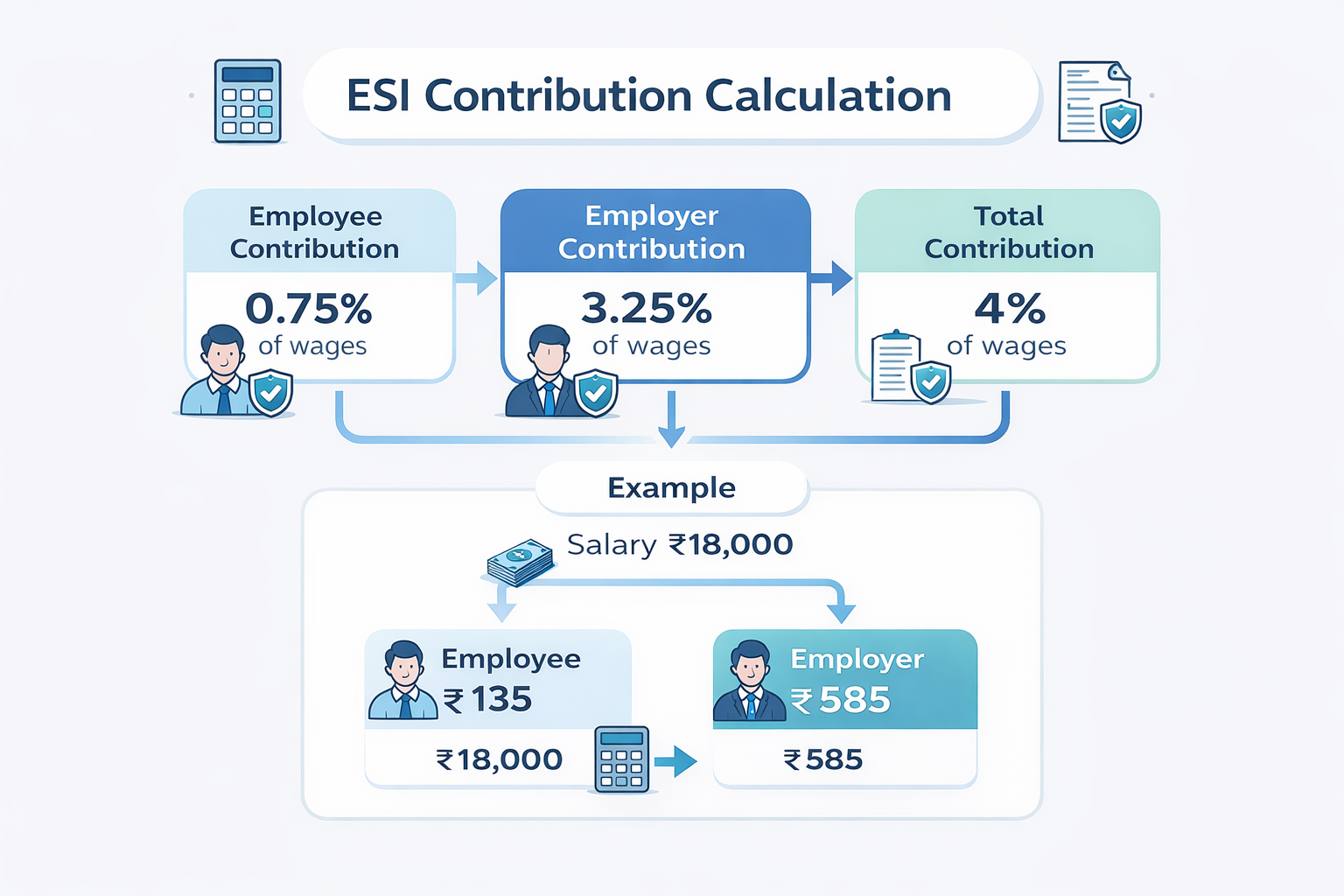

For example, if an employee’s gross monthly salary is ₹18,000, the employee contributes ₹135 (0.75%), the employer contributes ₹585 (3.25%), and the total ESI deposit becomes ₹720, which is reported and paid through the ESIC Social Security program system during the payroll cycle.

ESI Contribution Quick Summary

Employee contribution → 0.75% of wages

Employer contribution → 3.25% of wages

Total contribution → 4% of wages

Salary eligibility limit → ₹21,000 per month

These contribution rates are defined by the Employees’ State Insurance Corporation (ESIC) under the statutory insurance scheme.

What Is The Current ESI Contribution Rate For Employees And Employers?

The ESI contribution rate defines how much both the employee and the employer contribute toward the Employee State Insurance scheme each month. As per the current ESIC rules, the contribution is calculated as a percentage of the employee’s gross wages when the monthly salary is ₹21,000 or less.

The contribution is divided between the employee and the employer as follows:

Employee Contribution: 0.75% of gross salary

Employer Contribution: 3.25% of gross salary

Total Contribution: 4% of gross salary

The employer is responsible for deducting the employee’s share during payroll processing and depositing the combined contribution with the Employees’ State Insurance Corporation (ESIC) every month.

It is important to note that the ESI contribution rates were revised in July 2019. Before this revision, the employee contribution was 1.75% and the employer contribution was 4.75% of wages. The reduction was introduced to lower the compliance cost for employers while maintaining coverage under the ESI scheme.

Because the contribution percentage applies directly to wages included under these rules, understanding the current contribution rate and the wage components considered in the calculation is essential for accurate payroll processing and statutory compliance.

Which Salary Components Are Included In ESI Wages?

When calculating ESI contribution, employers must first identify which parts of an employee’s salary are treated as wages under these rules. In simple terms, the scheme considers most regular payments made to an employee for work performed. These salary elements form the base amount on which the contribution percentage is applied during payroll processing.

The following salary components are generally included when determining wages for ESI contribution.

However, certain payments are not treated as wages under the scheme, so they are not used while calculating the contribution amount.

How To Calculate ESI Step By Step (With Formula)

Calculating ESI contribution is simple once you know the employee’s monthly wages and the current contribution rates. As of 2026, employees contribute 0.75% of wages and employers contribute 3.25%, making the total contribution 4% of eligible wages. This calculation is usually done during monthly payroll processing.

Step 1: Identify Gross Wages

Start by identifying the employee’s gross wages eligible for ESI. These wages typically include components such as basic salary, dearness allowance, HRA, incentives, and overtime.

Employees are eligible for ESI if their monthly wages are ₹21,000 or less.

Step 2: Calculate Employee Contribution

Formula

Employee Contribution = Gross Wages × 0.75%

Step 3: Calculate Employer Contribution

Formula

Employer Contribution = Gross Wages × 3.25%

Step 4: Calculate Total ESI Contribution

Formula

Total Contribution = Employee Contribution + Employer Contribution

or

Total Contribution = Gross Wages × 4%

ESI Contribution Examples For Different Salary Levels

Understanding how the contribution amount changes with different salary slip levels can make the process much clearer. The examples below show how the employee share and employer share are calculated on monthly wages that fall within the ESI eligibility limit.

These examples show how the contribution amount increases as wages rise within the eligibility range. In practice, payroll systems calculate these amounts automatically before the employer submits the payment to the ESIC portal.

When Does ESI Coverage Apply And When Does It Stop?

Eligibility under the Employee State Insurance scheme is mainly based on an employee’s monthly wage level. In most cases, employees whose gross wages are ₹21,000 or less per month are covered under the scheme. For persons with disabilities, the wage threshold is slightly higher, allowing employees earning up to ₹25,000 per month to receive coverage.

Another important aspect of the scheme is the contribution period and benefit period structure. The contribution period runs from April to September and October to March.

The benefit period follows the contribution period and determines when employees can access benefits such as medical treatment, sickness benefits, and maternity support.

If an employee’s salary increases above ₹21,000 after enrollment, the employee remains covered until the end of the current contribution period. Once that period ends, contributions stop if the employee’s wages continue to remain above the eligibility threshold.

Understanding these rules helps payroll teams manage statutory deductions, eligibility checks, and ESIC compliance more accurately

Common Payroll Mistakes Companies Make With ESI Contributions

Even though the calculation method for ESI contributions is straightforward, mistakes often happen during payroll processing. Many of these errors occur because salary components are misunderstood or eligibility rules are not applied correctly. When contributions are calculated incorrectly, it can lead to compliance issues, incorrect deductions from employee wages, or delays in statutory filings.

Using The Wrong Salary Components

One of the most frequent payroll errors happens when incorrect salary elements are used while determining eligible wages. Payments such as basic salary, dearness allowance, incentives, overtime, and attendance bonuses are generally considered when calculating contributions. However, items like gratuity, retrenchment compensation, or leave encashment should not be included.

Continuing Deductions After Eligibility Ends in ESI Calculation

Another common issue occurs when deductions continue even after an employee’s wages move beyond the eligibility threshold. Employees who cross the wage limit remain covered only until the end of the current contribution period.

Incorrect Treatment Of Overtime Payments

Overtime payments are sometimes excluded or incorrectly added during payroll calculations. This can affect the final contribution amount and create discrepancies in compliance records.

Delays In ESIC Contribution Payments

Late deposits are another operational challenge. Employers must submit contributions to the ESIC portal within the prescribed time each month. Missing these deadlines can lead to penalties and interest charges.

Lack Of Regular Payroll Review in ESI Calculation

Without reviewing contribution records and wage classifications periodically, small calculation errors can continue for months. Regular payroll checks help ensure statutory obligations are handled correctly

Frequently asked Questions (FAQ’s)

What is the contribution rate under the ESI scheme?

Employees contribute 0.75% of wages, while employers contribute 3.25%.

What is the wage limit for eligibility?

Employees earning ₹21,000 or less per month are generally covered. For persons with disabilities, the limit is ₹25,000.

How is the contribution amount calculated?

Employee share = Gross wages × 0.75%

Employer share = Gross wages × 3.25%

Which salary components are counted as wages?

Basic salary, dearness allowance, HRA, incentives, overtime, and attendance bonus are usually included.

What happens if an employee’s salary increases above the limit?

Coverage continues until the end of the current contribution period, after which deductions stop if wages remain above the limit.